The Indian Drone Industry: A Ground-Up Deep Dive

From first principles to the India opportunity: what a drone actually is, who controls each link of the value chain, and the economics that decide the winners.

This is the text companion to the interactive deep dive on Nothing Linear, which includes scoring tools, sortable company tables, and visual breakdowns of the full value chain. If you prefer reading, you're in the right place. If you want to click around and explore, head there.

What Is a Drone?

A drone — formally an Unmanned Aerial Vehicle (UAV) — is an aircraft with no human pilot on board. But the word most people skip is the one that matters most: system.

The aircraft is only one part of a drone. When someone says a company “makes drones,” the genuinely interesting question is always which parts of the whole system it actually makes, and which it merely buys and bolts together.

A complete Unmanned Aircraft System (UAS) has five parts that must work together:

The Air Vehicle — the aircraft itself: frame, motors, flight controller and power. The part everyone pictures, but only one of five.

The Ground Control Station (GCS) — where the mission is planned and monitored. From a laptop running QGroundControl to a ruggedised military console.

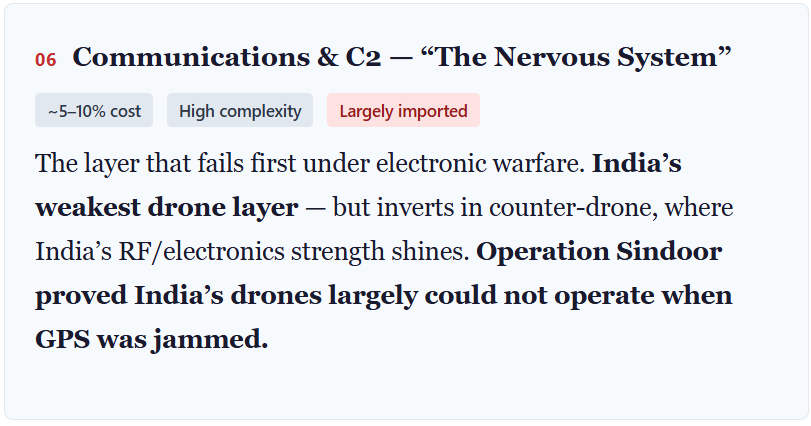

The C2 Datalink — the command-and-control radio link carrying instructions up and telemetry plus video down. The layer that fails first under electronic warfare.

The Payload — cameras, sensors, or munitions. The reason the drone flies at all.

The Operator / Autonomy — the human pilot, or increasingly, the autonomy stack that replaces that human.

The key insight: The drone is not the prize. The components and the software are the prize. Assembly — bolting together imported parts — is a commodity, and every company that forgot this lost, however impressive its hardware looked.

• • •

The Five Configurations

Not all drones look alike. Each configuration trades off endurance, hover capability, cost and mission fit:

Multirotor (quadcopters, hexacopters) — the most common form. They hover with precision and are mechanically simple, but trade endurance for that simplicity. The overwhelming majority of civilian drones. India: IoTechWorld Agribot, ideaForge Q-series, Aurelia A4/A6.

Fixed-wing — miniature aeroplanes. Long range and endurance, efficient ground coverage, but they cannot hover. Used for long-range mapping and military ISR. India: Aereo/Aarav, NewSpace MAPSS.

Hybrid VTOL — the fastest-growing configuration. Takes off vertically, then transitions to efficient fixed-wing flight. Grand View expects this segment to grow at the highest CAGR of any product type — above 12% — through 2033. India: Dynauton CHEEL, TechEagle Vertiplane X3.

Single-rotor / unmanned helicopter — heavy-lift platforms with efficient hover. India: EndureAir hydrogen fuel-cell UAVs, BonV Aero high-altitude resupply.

FPV (First-Person-View) — small, fast, agile quadcopters flown “through the camera” with goggles. Made consumable by the Ukraine war — produced and expended by the million. The defining attritional weapon of modern war. India: Apollyon Dynamics.

• • •

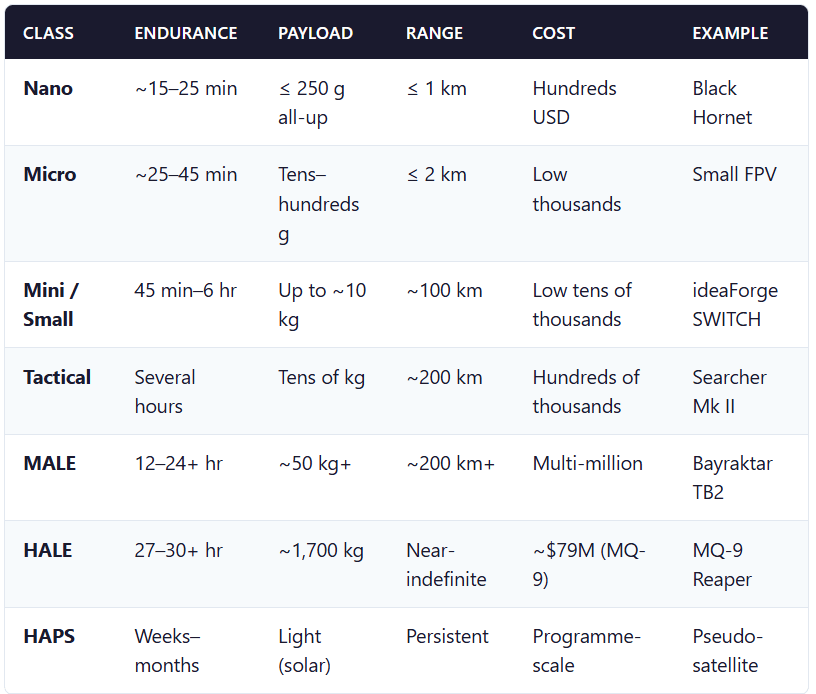

The Altitude Ladder: Palm-Sized to Stratospheric

Most Indian startups play in the Mini/Small class (DGCA Small = 2–25 kg). The tactical and above tiers are where the real defence money sits. India formalised a 31-platform HALE-class buy (MQ-9B) in October 2024 and approved a ~₹15,000-crore HAPS programme in February 2026.

• • •

Why Drones Exist: The Three Advantages

Strip away the hype and a drone does exactly one thing: it decouples a sensor or payload from the cost, risk and physical limits of putting a human in the air.

1. Cost Asymmetry

A camera that once needed a crewed helicopter — at lakhs of rupees per flight hour, plus pilot, fuel and risk — now flies on a machine costing two to three lakh rupees or far less, collapsing the cost of aerial data by one to two orders of magnitude.

In war the asymmetry becomes staggering: a first-person-view (FPV) drone costing a few hundred dollars can destroy a main battle tank costing two to five million dollars. No weapon system in modern history has offered that exchange ratio.

2. Risk Removal

Drones excel at the missions militaries and industries call “dull, dirty, and dangerous.” Patrolling a border, inspecting a high-voltage power line, spraying pesticide, entering a collapsed building, flying into contested airspace — none of these any longer requires risking a human life.

3. Data Persistence

A drone generates dense, repeatable, geo-tagged data — multispectral maps of crop health, centimetre-accurate 3D survey models, real-time intelligence feeds — and it can loiter far longer and far more cheaply than a crewed aircraft.

The Smartphone Insight

These advantages crossed an economic threshold in the mid-2010s for one specific reason: the same component revolution that produced the smartphone — cheap MEMS gyroscopes, dense lithium batteries, efficient brushless motors, commodity GPS chips and high-resolution camera modules — is exactly what made reliable, affordable drones possible.

A drone is, in a real engineering sense, a flying smartphone. This is also the deep reason China — the workshop that builds the world’s smartphones — came to dominate drones. The two facts are the same fact.

• • •

Why Now: The Five Events That Made This Industry

2013 — DJI Phantom Launches

DJI’s Phantom made aerial photography mass-market and effectively created the consumer drone category. A commercial boom followed, then a brutal shakeout that wiped out almost every Western competitor.

“DJI’s dominance exceeds even Apple’s grip on smartphones.”— Disruption Radar, 2026

2020 — Nagorno-Karabakh

Azerbaijani Bayraktar TB2 drones destroyed Armenian armour and air-defence systems on video, proving that comparatively cheap drones could decide a conventional war between states.

“Drones are the biggest disruption to warfare since Genghis Khan put stirrups on horses.”— Erik Prince, Disruption Radar, 2026

2022 — Ukraine

The defining event of the modern industry. Drones became consumable munitions used at genuinely industrial scale — produced and expended by the million, not maintained as durable equipment. Ukraine built ~5 million drones in the last year. Russia launched 805 in a single night.

“Modern battlefields consume drones the way 20th-century conflicts consumed artillery shells: by the thousands, every day.”— Fox News, June 2026

2025 — Operation Sindoor

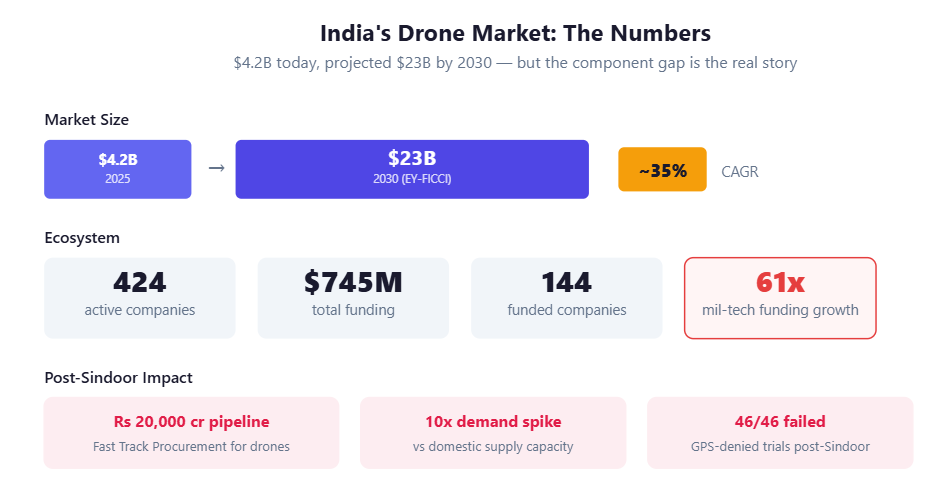

In the May 2025 India–Pakistan conflict, both sides deployed drones at scale despite owning advanced jets and missiles. Government demand spiked to roughly 10× domestic supply overnight. In post-Sindoor trials, all 46 tested manufacturers failed GPS-denied conditions. It exposed India’s component dependence and triggered a procurement surge.

“The recent reports of a fresh procurement outlay of approximately INR 20,000 crore signal a strong, multi-year demand tailwind.”— Ankit Mehta, CEO, ideaForge, Q4 FY26 earnings call

2025 — US “Drone Dominance” Executive Order

Policy money became the rocket fuel. A US FY2026 defence budget with $13.6bn for autonomous systems, India’s ~₹20,000-cr procurement pipeline, and Ukraine’s BRAVE-1 all signalled that government demand, not venture capital, now drives the industry.

• • •

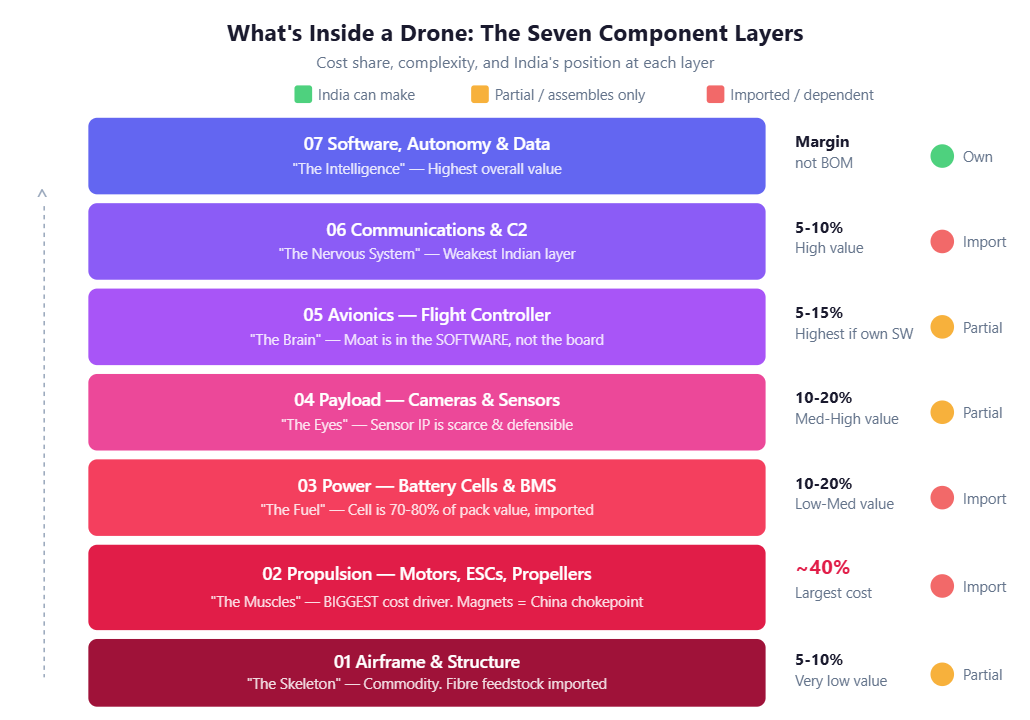

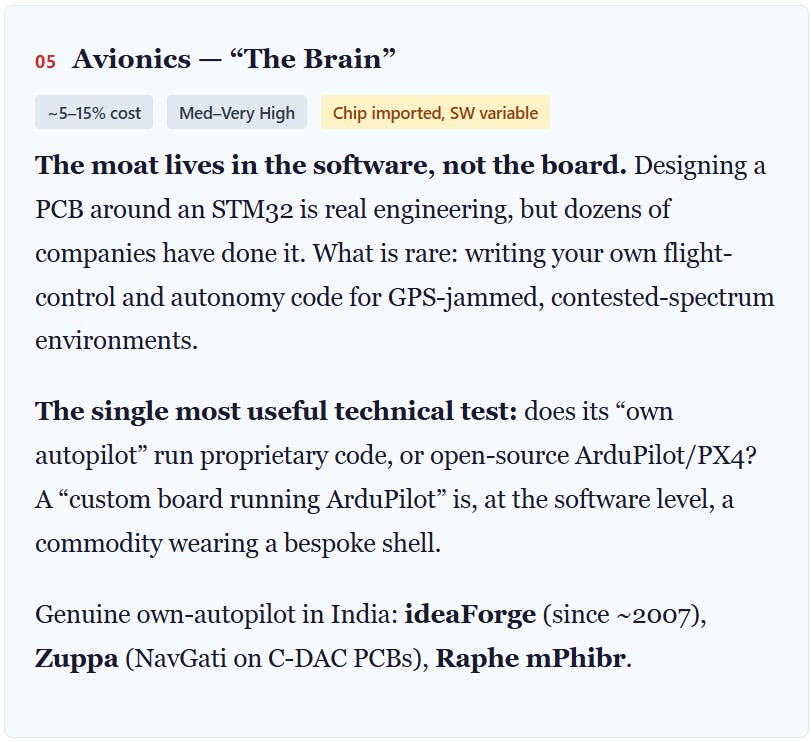

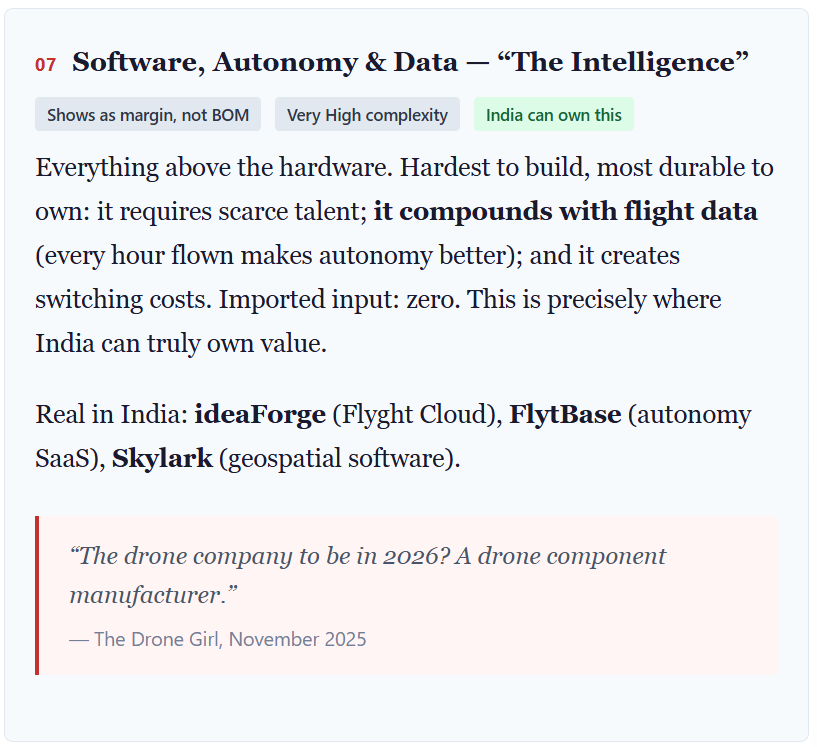

The Seven Components: What’s Actually Inside a Drone

This is the section that separates the people who understand the industry from the people who don’t. Every drone is built from seven component layers. Understanding who controls each one — and where the value concentrates — is the entire game.

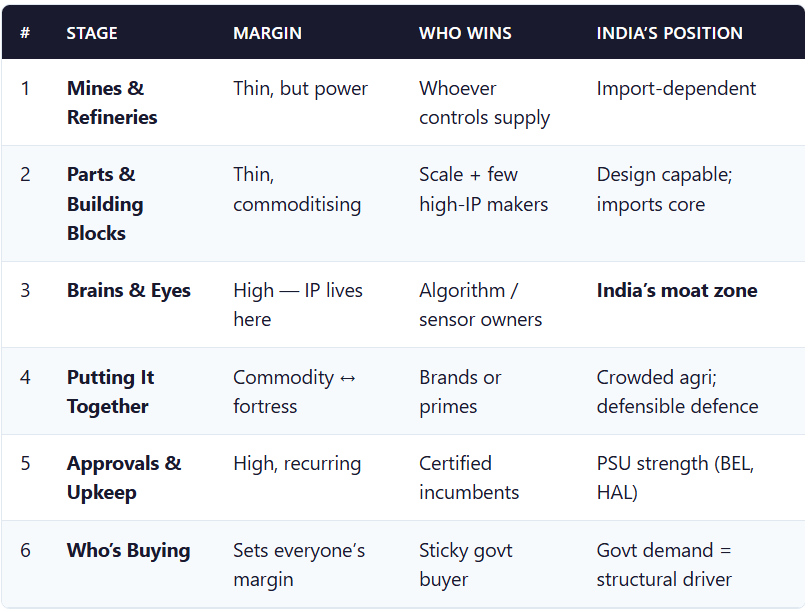

The Value Chain: Six Stages from Mine to Mission

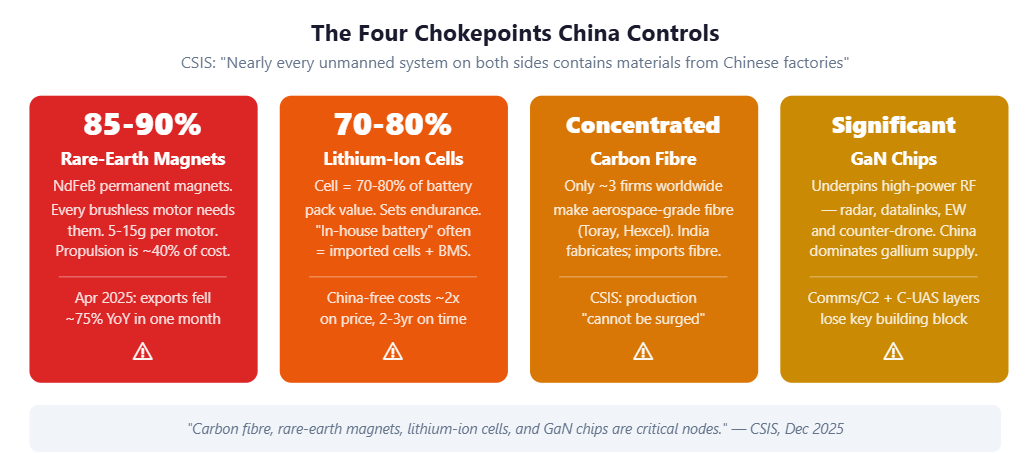

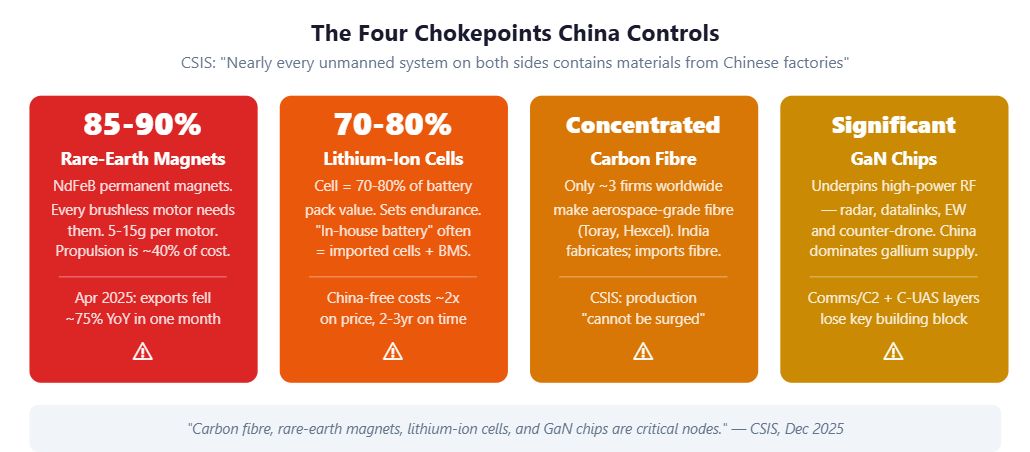

The Four Chokepoints: Where China Can Throttle the World

“Every drone involved in the war in Ukraine depends on China. From palm-sized quadcopters to long-range loitering munitions, nearly every unmanned system on both sides contains materials and components that originate in Chinese factories and refineries.”— CSIS, December 2025

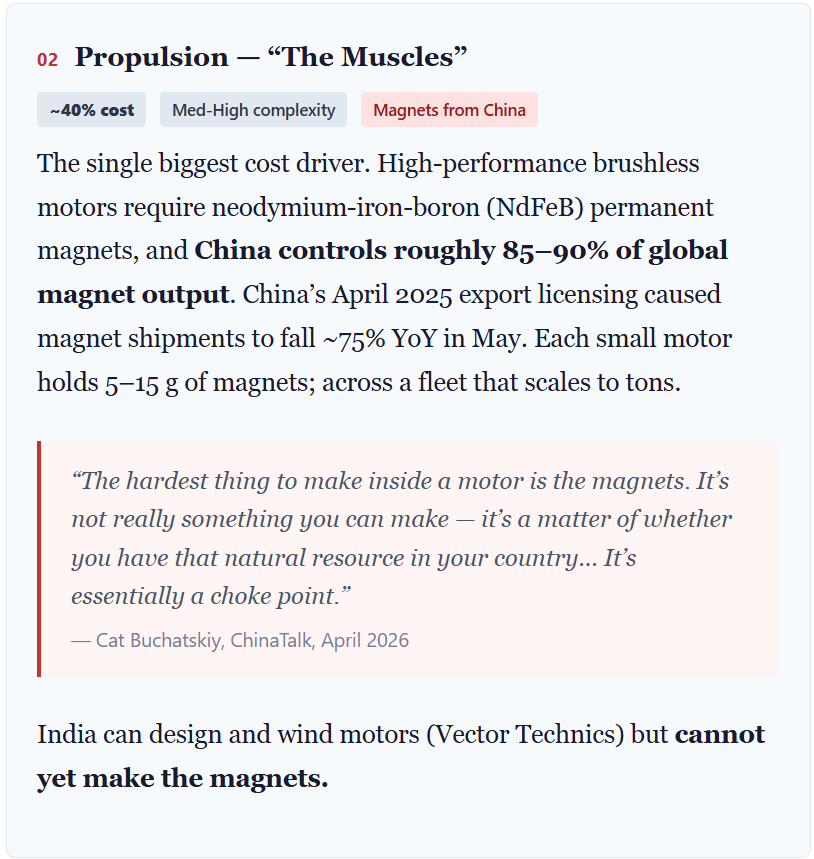

1. Rare-Earth Magnets (NdFeB) — China controls 85–90%

Every high-performance brushless motor needs them. Each small motor holds 5–15 g; across a fleet that scales to tons. China’s April 2025 export licensing caused magnet shipments to fall ~75% YoY. The Pentagon took a $400M equity stake in MP Materials. In India, this is the single highest-value localisation target.

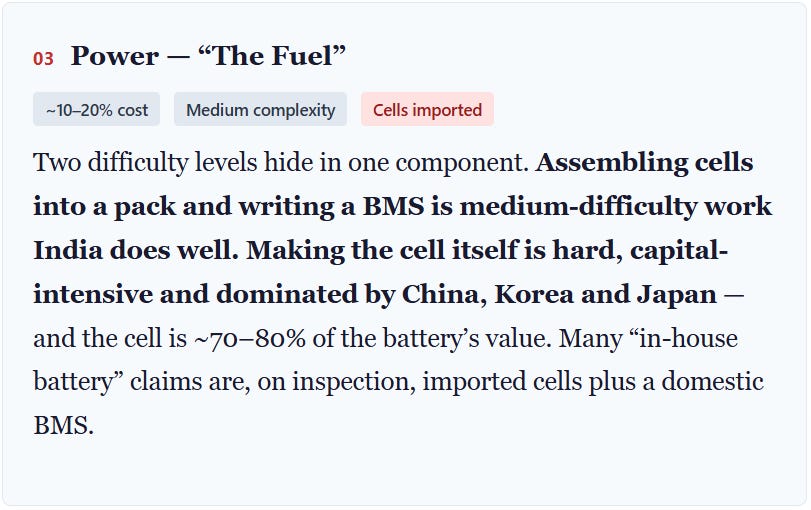

2. Lithium-Ion Cells — China dominant (with Korea & Japan)

The cell is ~70–80% of a battery pack’s value. Making the cell is hard and capital-intensive. Going China-free costs roughly 2× on price and 2–3 years on time.

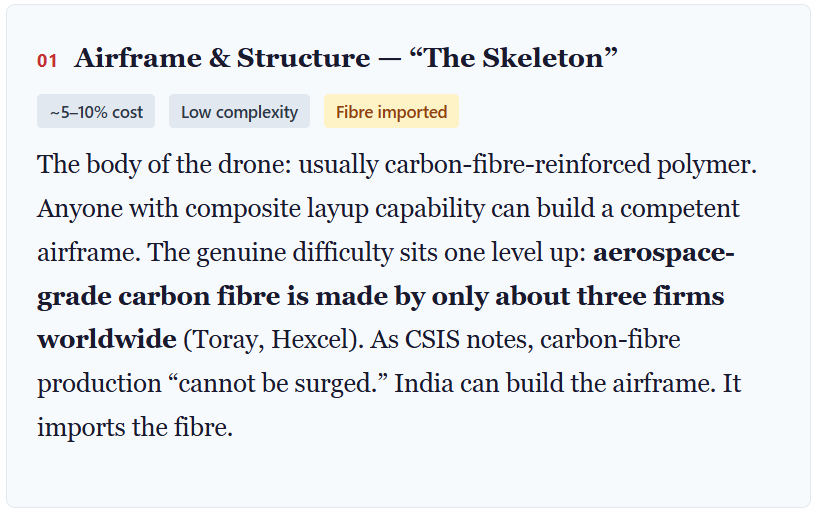

3. Carbon Fibre — Toray, Hexcel + few others

Anyone can lay up a frame, but the raw fibre is made by only about three firms worldwide. Even a fully domestic airframe sits on a foreign material choke point. CSIS: production “cannot be surged.”

4. Gallium-Nitride (GaN) Chips — China dominates gallium supply

GaN underpins high-power RF — radar, datalinks, electronic warfare and counter-drone systems. If this is cut, the comms/C2 and counter-drone layers lose their highest-performance building block.

“At least 80,000 components across 1,900 U.S. weapons systems depend on Chinese-sourced rare earths.”— PR Newswire / Morningstar, May 2026

• • •

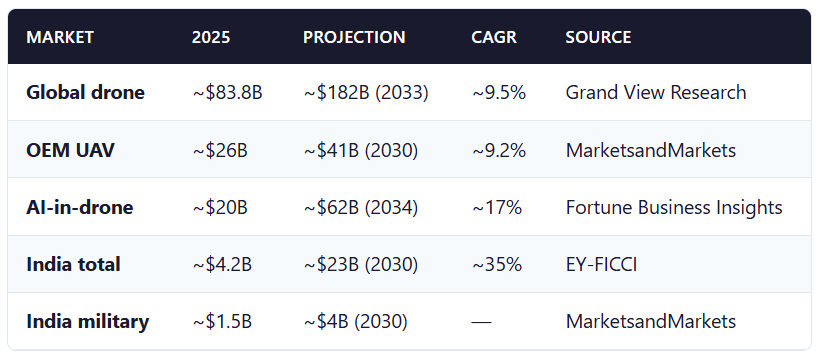

Supply & Demand: The Numbers

The Ukraine reset: These numbers don’t capture the most important shift. Drones are no longer durable equipment — they are consumable munitions. Ukraine built ~5 million drones in the last year. Drones account for >90% of Russian battlefield losses. A Chinese motor costs ~$70; the Ukrainian equivalent runs ~$150. At 9,000 drone deployments per day, those cost gaps matter enormously.

“Investment value is migrating from drone brands to component suppliers: propulsion systems, secure electronics, magnet makers, rare-earth processors, and battery suppliers… The new moat is not just software or flight performance. It is traceability.”— RareEarthExchanges, May 2026

India: 424 active companies, $745M total funding, 144 funded (Tracxn). Military-tech funding rose 61-fold in a decade — from $3.1M (2016) to $192.4M (2025).

• • •

The Global Giants: Who Won and Why

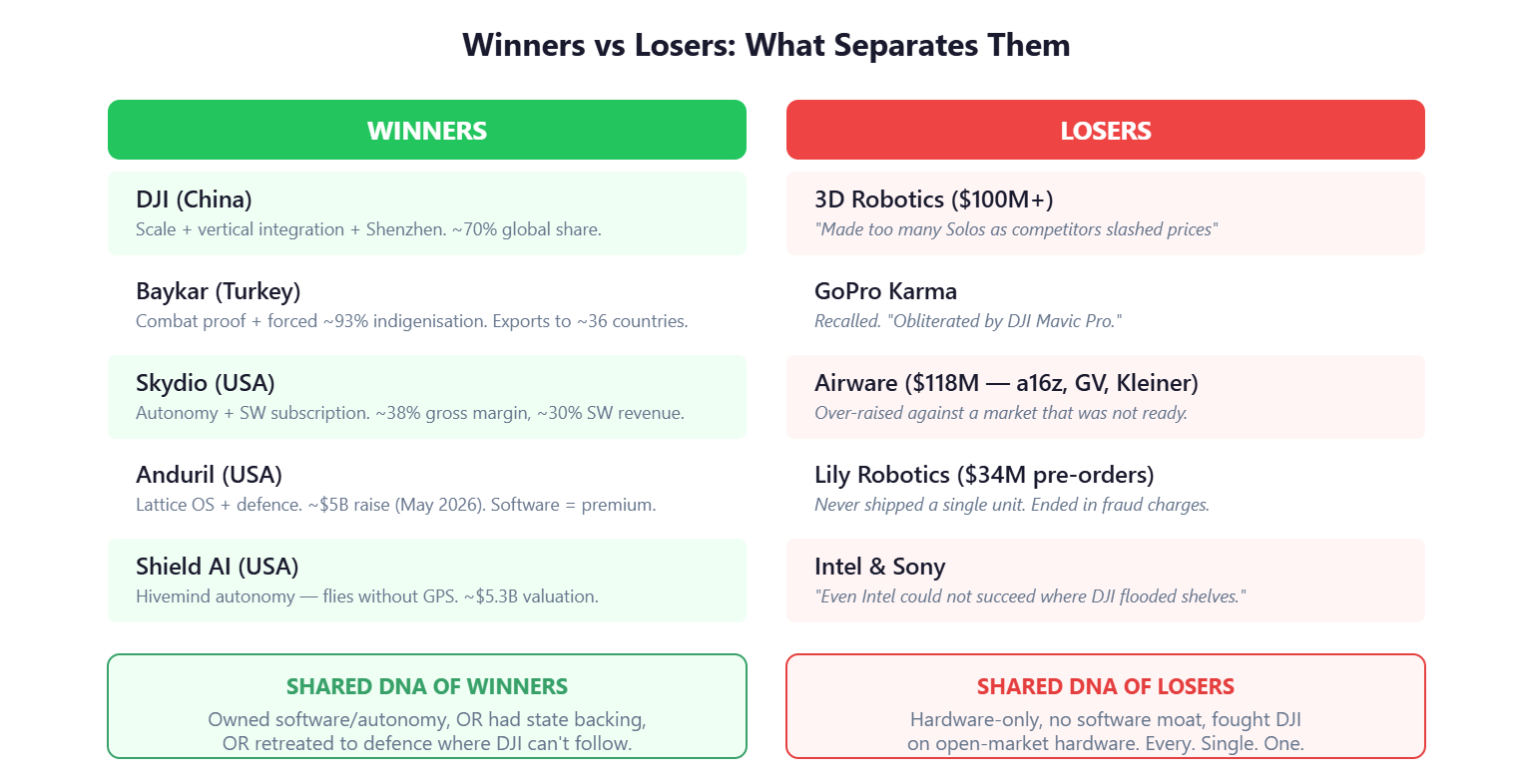

DJI (China) — The Benchmark

~70% of the global market, ~80% of the US market. Won through vertical integration, Shenzhen manufacturing scale, relentless iteration, and price-performance no competitor could match. The lesson: you do not beat DJI on open-market hardware.

Baykar (Turkey) — The Playbook India Should Study

Combat proof first (Nagorno-Karabakh 2020); forced deep indigenisation (US export ban compelled ~93% localisation, and that forced sovereignty became the moat); state backing; continuous EW-resilience leaps. The most instructive case for India.

Skydio (USA) — Survive by Retreating

Conceded consumer/commercial entirely. Retreated to defence where DJI is restricted. ~$562M raised; $1.2B bookings; ~38% gross margin; ~30% software revenue. Hardware gets you in the door; software makes the money.

Anduril + Shield AI (USA) — Software Eats the Drone

Anduril (~$5B raise, May 2026) and Shield AI (~$5.3B valuation) prove that the autonomy and software layer — not the airframe — commands the premium.

The Graveyard

Winners — shared DNA

Owned software/autonomy OR had state backing

Retreated to defence where DJI can’t follow

Sovereignty / traceability as moat

Capital built copy-resistant IP, not commodity hardware

Losers — shared DNA

3D Robotics ($100M+) — overbuilt into price collapse

GoPro Karma — recalled; obliterated by DJI Mavic

Airware ($118M) — over-raised, market not ready

Lily ($34M pre-orders) — never shipped a single unit

Intel & Sony — both entered, both retreated

Every single one tried to beat DJI on open-market hardware. Every single one failed.

• • •

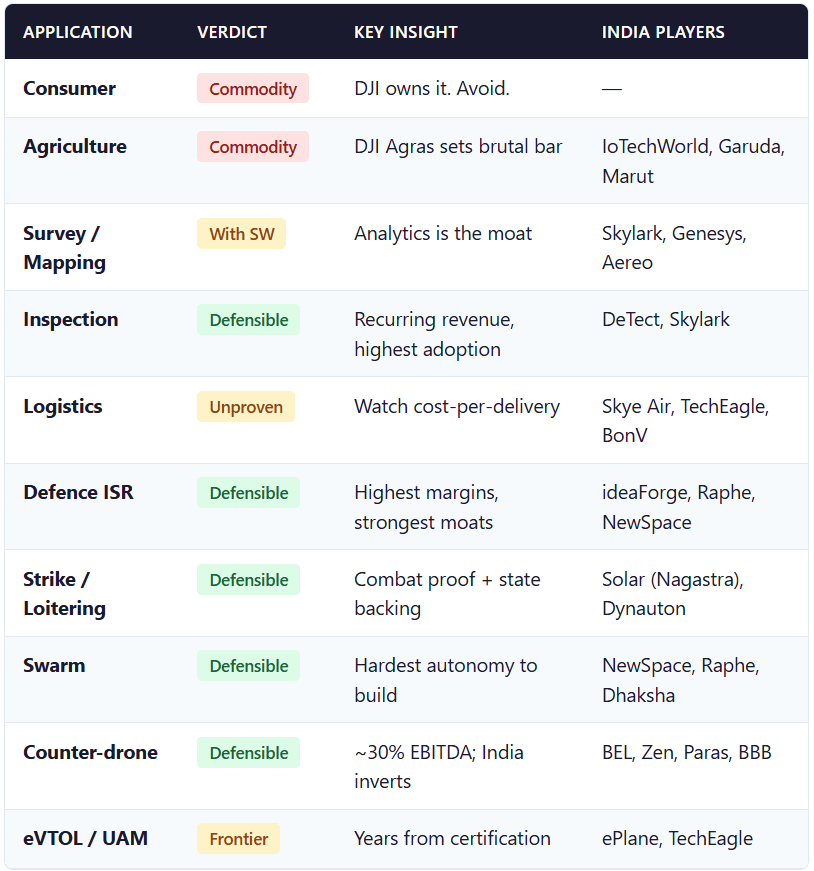

End Uses: Where the Money Is

India’s RF/electronics/optics strength inverts its component weakness in counter-drone — the country may end up stronger at stopping drones than building them.

India: Before and After Sindoor

India’s drone industry has a clear before and after. In Operation Sindoor (May 2025), both sides deployed drones at scale. Government demand spiked to ~10× domestic supply. All 46 tested manufacturers failed GPS-denied conditions.

“The Army has inducted loitering munitions, kamikaze and surveillance drones for over Rs 5,000 crore post Operation Sindoor… A larger Rs 20,000 crore Fast Track Procurement for drones is likely in 2026.”— ThePrint

The Policy Stack

Drone Rules 2021 — weight classes, UIN, NPNT, DigitalSky

Import ban on finished drones (2022) — the measure that created India’s assembly industry

PLI Scheme (~₹2,000 cr) — production-linked incentives

GST cut to 5% (Sept 2025) — lowered adoption cost

Mission Drone Shakti (~₹1,600–1,800 cr / 5 years) — first scheme targeting components

Buy-Indian IDDM (DAP 2026) — procurement tilted toward indigenous systems

The Component Gap

India largely ASSEMBLES drones; it does not yet MANUFACTURE the critical components inside them. Roughly 45–55% of critical components by value are imported — closer to 60–80% for the highest-value parts (flight-controller chips, sensors, rare-earth magnets, battery cells, RF modules).

When a company claims a high “indigenisation percentage,” always ask: by part-count, or by cost? The marketing counts the easy layers; the hard layers are where the truth lives.

• • •

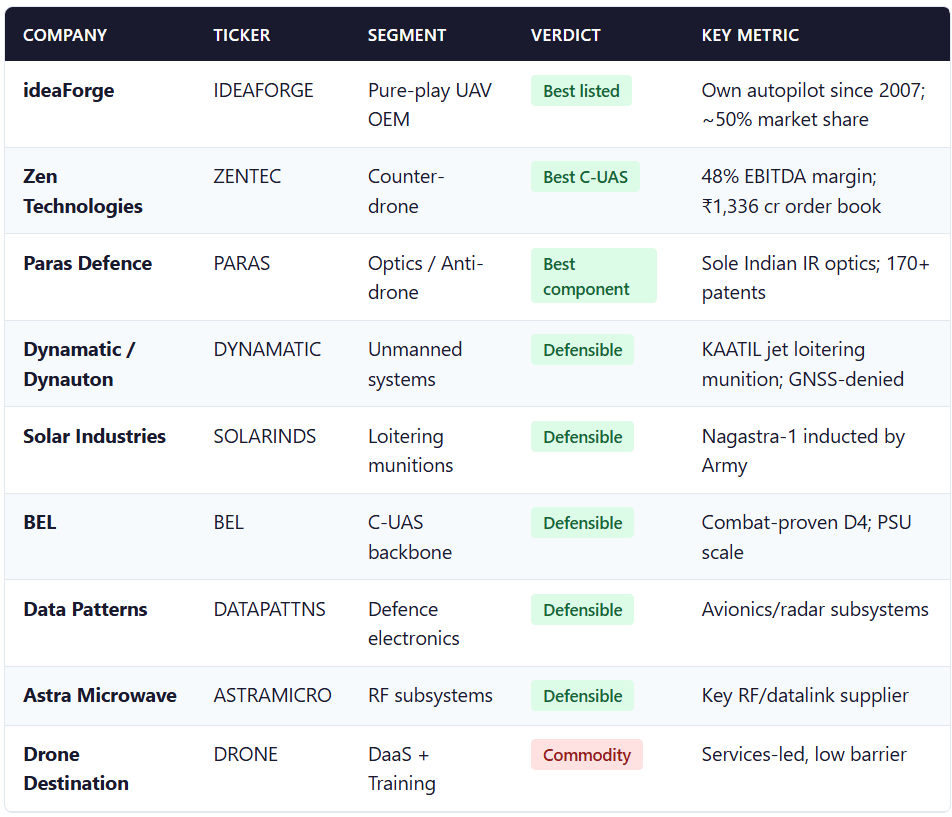

Indian Companies: Who’s Building What

Listed Companies

Unlisted Companies

Raphe mPhibr — $154M raised

The closest Indian analogue to a Baykar-style sovereign builder. Deepest genuine vertical integration: own flight controllers, autopilot, inertial navigation, batteries, composites and wire harnesses. Zero China parts. Candid that it still imports only radar and high-end cameras. 600+ staff; deployed in Operation Sindoor. $100M Series B by General Catalyst — the largest private raise in Indian drone history.

“This funding is more than an investment; it is a commitment to build in India what the country can no longer afford to import.”— Raphe mPhibr

NewSpace Research — $73.2M raised

India’s swarm leader. Delivered the country’s operational 100-drone swarm to the Army; ₹168 cr MAPSS contract (India’s first solar-powered surveillance drone).

Zuppa Geo Navigation

One of very few Indian firms with a genuine proprietary autopilot (NavGati on C-DAC PCBs). Claims to be among only ~7 companies globally with its own autopilot technology. The “Intel of drones.”

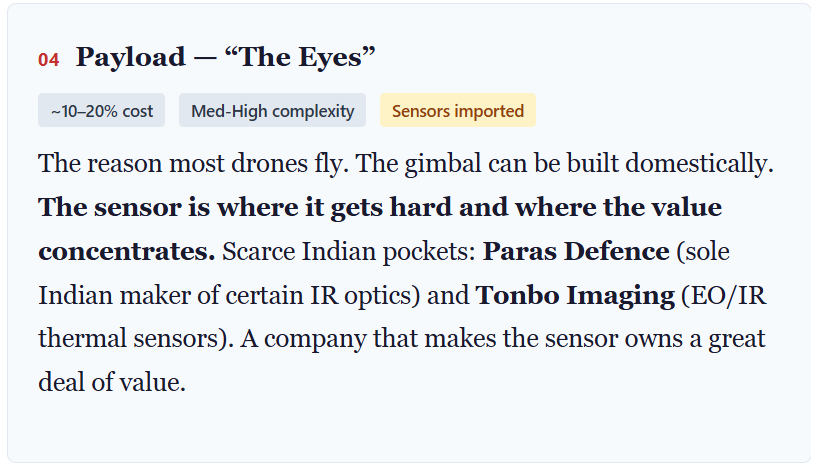

Tonbo Imaging — $20.4M raised

The critical “eyes” supplier. Proprietary EO/IR thermal sensor IP — one of the genuinely scarce, defensible niches in the whole value chain.

Big Bang Boom Solutions — $29.9M raised

Largest startup C-UAS order (₹200 cr+ iDEX). Defensible passive-RF counter-drone IP in the highest-margin niche.

Garuda Aerospace — $49.5M raised

Best agri/DaaS scale-and-brand play, but ~45–55% of components imported. Invested in Zuppa precisely to acquire autopilot depth. MS Dhoni-backed.

Also notable

FlytBase — pure software/autonomy SaaS. Skylark — geospatial intelligence (Spectra). BonV Aero — high-altitude cargo above 18,000 ft. EndureAir — hydrogen propulsion. AKSI Aerospace (2024, Hyderabad) — interesting subsystem-breadth play (own autopilot, motors, cameras, batteries); ₹85 cr FIXAR deal; very early-stage.

• • •

The Mental Model: Six Questions for Any Drone Company

Moat type — does it have scale, autonomy/software IP, or combat-proof plus state backing? If none: likely a future corpse.

Battlefield choice — open market or protected niche? Fighting DJI on open hardware is usually fatal.

Make vs assemble — what share of cost and critical components does it genuinely own? High “indigenisation %” on imported chips, magnets and cells is a red flag.

Sovereignty under stress — could it keep producing if China cut off magnets, cells and chips tomorrow?

Capital discipline — is the money building copy-resistant IP or subsidising commodity hardware?

Buyer durability — is there a sticky, repeat, well-funded customer (ideally a government)?

• • •

The Field: In Their Own Words

“Every drone involved in the war in Ukraine depends on China.”— CSIS, December 2025

“Drones account for more than 90 percent of Russian battlefield losses.”— Maj. Robert ‘Magyar’ Brovdi, Commander, Ukraine’s Unmanned Systems Forces, NYT, March 2026

“Our biggest FPV primes took 2 to 3 years to get things up and running… purely state contracts and bootstrapped companies… we didn’t really have VC in Ukraine at all.”— Cat Buchatskiy, ChinaTalk, April 2026

“A Chinese motor costs around $70; the Ukrainian equivalent from Motor-G runs about $150. At 9,000 drone deployments per day, those cost gaps matter enormously at scale.”— DroneXL, March 2026

“Raphe mPhibr produces its own flight controllers, batteries, and all components and materials required to build drone structures… the startup does not rely on China for any of the components it uses.”— TechCrunch, June 2025

“We got knocked down for a really simple reason: We made too many Solos, especially given how fast our competitors dropped prices and flooded the market.”— 3D Robotics founder

• • •

The Takeaway

The drone industry is no longer about the drone. It’s about the components, the software, and the sovereignty to keep building when supply chains are weaponised.

The winners will own one of three moats: manufacturing scale plus vertical integration (DJI), proprietary autonomy and software (Anduril/Shield AI), or combat proof plus state backing (Baykar).

The losers will be the ones fighting DJI on open-market hardware, assembling imported parts without owning any critical layer, and calling that “indigenisation.”

For India: the country assembles drones; it does not yet manufacture the critical components inside them. The post-Sindoor procurement surge (~₹20,000 cr pipeline), Mission Drone Shakti, and global demand create a window. But the window is in components and software, not in assembly.

The capability that now matters most, and that almost no one in India has, is EW-resilient, GPS-denied autonomy. That is where the durable value of this industry is migrating, and it is the hardest thing to copy.

This is just one deep dive

Nothing Linear tracks 4,000+ Indian stocks across 75 sectors in real time — heatmaps, indices, commodities, currencies, macro data, and more research like this.

Explore the interactive version

This deep dive comes with scoring tools, sortable company tables, and visual value-chain breakdowns on Nothing Linear.

Open the Interactive Deep Dive →

Sources: CSIS (The Drone Supply Chain War, Dec 2025), RUSI (Drones: Decoupling Supply Chains, Nov 2025), Grand View Research (Drone Market 2026–2033), EY-FICCI (Making India the Drone Hub, 2025), MarketsandMarkets, Fortune Business Insights, Tracxn (424 companies, $745M funding), ideaForge Q4 FY26 earnings call, Zen Technologies Q2 FY26 call, ChinaTalk (How Ukraine Scaled, Apr 2026), RareEarthExchanges, Fox News, DroneXL, TechCrunch, ThePrint, PR Newswire/Morningstar, DRONELIFE, PIB/DGCA DigitalSky, and company filings.